Japanese tax system is very complicated therefore a lot of people would leave it to the tax accountants. But I think that getting knowledge about the tax system is useful and it is the same condition also for foreign workers living in Japan.

1. Employment income tax system

Employment income of foreign employees working in Japan is subject to two kinds of taxation.

One of them is income tax(national tax)which is administered by local taxation offices.

The other is inhabitant tax(local tax) which is administered by municipal offices.

2.The income tax

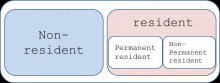

The taxation methods and scope of taxable income are different that of depending on whether an employee is a "resident" or "non-resident".

A foreign national who has "domicile(core base of life)" or has had residence(place to live other than domicile ) for one year or longer in Japan, is regarded as a "resident" in terms of the tax code, and he/she is subject to income tax with the same rate as Japanese amployees.

However, a salary earner is regarded as "resident" immediately after entering Japan unless his/ her employment contract, etc.,identifies(that the period of stay) is less than one year in advance.

日本の税制度は非常に複雑で、専門家に丸投げという方も多いかと思います。

でも、税についての知識を持つことは自身の生活のためにも役立ちます。それは日本に住む外国人労働者の方にも同じことが言えるのです。

1.給与所得にかかる税制度

日本で働く外国人の給料にかかる税金には、国税である所得税と地方自治体の税金である住民税の2種類があります。所得税は税務署、住民税は市区町村が窓口になります。

2.所得税

日本では、給与所得に対する所得税については、給与の支払者(事業主)が支払いを受ける者(労働者)に代わって所得税を徴収し国に納めるという、「源泉徴収制度」を採用しています。給与を支払う事業主には、源泉徴収が原則的に義務付けられています。

さらに「居住者」と「非居住者」の区分があり、課税方法と課税対象範囲が異なっています。

<居住者の税金>

居住者と非居住者

日本国内に「住所(生活の拠点)」を有するか、または国内に現在まで引き続いて1年以上「居所(住所以外の現実に居住する場所)を有する外国人は税法上「居住者」とされ、日本人と同じ税率の所得税が課税されます。ただし、給与所得者については、居住期間が1年未満であっても、労働契約等で滞在期間があらかじめ1年未満であることが明らかな場合を除いては、入国後直ちに「居住者」と推定されます。

Harumi Miyahara

Uchiyama FP Office Co;Ltd.

1. Employment income tax system

Employment income of foreign employees working in Japan is subject to two kinds of taxation.

One of them is income tax(national tax)which is administered by local taxation offices.

The other is inhabitant tax(local tax) which is administered by municipal offices.

2.The income tax

The taxation methods and scope of taxable income are different that of depending on whether an employee is a "resident" or "non-resident".

A foreign national who has "domicile(core base of life)" or has had residence(place to live other than domicile ) for one year or longer in Japan, is regarded as a "resident" in terms of the tax code, and he/she is subject to income tax with the same rate as Japanese amployees.

However, a salary earner is regarded as "resident" immediately after entering Japan unless his/ her employment contract, etc.,identifies(that the period of stay) is less than one year in advance.

日本の税制度は非常に複雑で、専門家に丸投げという方も多いかと思います。

でも、税についての知識を持つことは自身の生活のためにも役立ちます。それは日本に住む外国人労働者の方にも同じことが言えるのです。

1.給与所得にかかる税制度

日本で働く外国人の給料にかかる税金には、国税である所得税と地方自治体の税金である住民税の2種類があります。所得税は税務署、住民税は市区町村が窓口になります。

2.所得税

日本では、給与所得に対する所得税については、給与の支払者(事業主)が支払いを受ける者(労働者)に代わって所得税を徴収し国に納めるという、「源泉徴収制度」を採用しています。給与を支払う事業主には、源泉徴収が原則的に義務付けられています。

さらに「居住者」と「非居住者」の区分があり、課税方法と課税対象範囲が異なっています。

<居住者の税金>

居住者と非居住者

日本国内に「住所(生活の拠点)」を有するか、または国内に現在まで引き続いて1年以上「居所(住所以外の現実に居住する場所)を有する外国人は税法上「居住者」とされ、日本人と同じ税率の所得税が課税されます。ただし、給与所得者については、居住期間が1年未満であっても、労働契約等で滞在期間があらかじめ1年未満であることが明らかな場合を除いては、入国後直ちに「居住者」と推定されます。

Harumi Miyahara

Uchiyama FP Office Co;Ltd.